|

|

|

|

|

|

|

EGG‑NEWS.com

Egg Industry News, Comments & More by

Simon M.Shane

|

|

|

|

|

|

|

Editorial

Epidemiologic Evaluation of Bovine Influenza Apparently Obstructed by States

|

05/14/2024 |

|

From a statement issued by Dr. Nirav Shah, Principal Deputy Director of the Center for Disease Control and Prevention (CDC), there is unanimity between his agency and USDA but state agricultural departments and individual dairy operations are obstructing investigations relating to the prevalence of infection in herds and workers. From a statement issued by Dr. Nirav Shah, Principal Deputy Director of the Center for Disease Control and Prevention (CDC), there is unanimity between his agency and USDA but state agricultural departments and individual dairy operations are obstructing investigations relating to the prevalence of infection in herds and workers.

With an emerging infection such as bovine influenza-H5N1 it is critical to determine as rapidly as possible the prevalence rate and geographic extent of the infection. Both field and molecular data must be obtained and analyzed to ascertain the rate of spread and modes of infection in order to implement counter measures. Epidemiologic data can be used to predict the progress of the disease in cattle and genomic evaluation can assess the risk of extension to the human population.

The CDC, with their focus on human health, is obviously concerned over the possible incidence rate of H5N1 infection among workers and should be allowed to conduct surveys. Texas Agriculture Commissioner Sid Miller stated, “They don’t need to do that, it’s overreach.” With respect to Commissioner Miller, he is in no position to comment on the epidemiologic realities of emerging disease and apparently is oblivious to the potential of extension to humans, although only one diagnosed case has been documented. Anecdotal reports by veterinarians visiting affected dairy herds suggest that individual workers demonstrated influenza-like symptoms including conjunctivitis. Colorado with only one case is following 70 workers to establish infection and possible transmission to contacts. Based on data from the CDC only 220 farm workers have been monitored for symptoms suggesting that only 150 workers have been evaluated among eight states where outbreaks have occurred. Texas with the most cases among dairy farms reported has only tested 20 workers with clinical signs and the results of diagnostic procedures have not been released. PCR assay results are available within 24 hours!

It is now five weeks since the index case of bovine influenza was diagnosed. Preliminary studies on the sequencing of isolates of H5N1 belatedly released by USDA-APHIS suggest that the disease has been present in dairy herds since late December 2023. To date there has been no structured evaluation of H5N1 prevalence among dairy herds on a national basis and the appropriate epidemiologic surveys on workers have not been conducted. This is despite the presence of RNA consistent with H5 influenza virus in both milk and wastewater especially in areas where outbreaks in dairy herds have occurred.

The World Health Organization has designated H5N1 avian influenza virus as a potential pandemic strain. The Agency has urged surveillance including documentation of outbreaks in avian and now mammalian species and the WHO maintains a database of outbreaks and the library of genomic sequences. The World Health Organization has designated H5N1 avian influenza virus as a potential pandemic strain. The Agency has urged surveillance including documentation of outbreaks in avian and now mammalian species and the WHO maintains a database of outbreaks and the library of genomic sequences.

The parochial but understandable concern of state departments of agriculture as expressed in their desire to protect the milk industry is self-evident. This standpoint obviously conflicts with the greater need to understand the epidemiology of bovine influenza-H5N1 and to develop a national program to limit infection. Of greater concern is the possible extension of a mutant virus to workers and then to the general population. The distribution of PPE is perhaps an initial step in preventing infection but will be difficult to implement given the underlying deficiencies in structural and operational biosecurity in comparison to egg-production complexes. Practical and cultural issues exist with the deployment and use of PPE that requires availability and acceptance. We need to know the numbers of workers that may have been infected from an affected herd, the duration of the clinical phase and of viral shedding. Surveillance based on molecular epidemiology including gene sequencing will be critical to timeously detect mutations that may contribute to infection of humans and person-to- person spread. It is understood that up to $98 million will be distributed by the USDA to provide 3,500 dairy farms with up to $28,000 to “contain the spread of the virus between animals and humans and for testing milk and animals for the virus” This commentator suggests that grants should be conditional on cooperation with federal agencies with respect to herd and worker surveillance.

We are not China. We should not suppress necessary epidemiologic investigations or the data collected. Bovine influenza-H5N1 and its avian counterpart will not simply go away, irrespective of the intensity of hope, denial and prayer. Fortunately it appears that the risk of contracting H5N1 from direct contact with cattle is minimal but this assumption is based on the current circulating virus and inadequate surveillance. Pasteurization obviously destroys the virus that is secreted into milk from infected mammary tissue. A mutation in the viral genome could profoundly alter present circumstances and could result in widespread infection as with “swine flu”. Dr. Shah notes, “We have all seen how a virus can spread around the globe before public health is even had a chance to gets shoes on, that’s a risk and one we have to be mindful of.” It is not what we know that has the potential to hurt the industry and population—but what we do not know.

The dairy industry, state agriculture organizations, and federal agencies including USDA-APHIS and the CDC should cooperate according to a coordinated and agreed plan to determine the extent of bovine infection following “One Health” principles. Currently the risk of mutation to a strain capable of infecting humans is very low based on accumulated knowledge. We are however in a situation of confronting a condition with a low probability of an adverse outcome for humans but with an extreme potential for morbidity and mortality and devastation of the Nation’s economy in a worst case scenario. Let us learn from our unfortunate experience with COVID from 2019 onwards and not underrate the significance of the infection at a stage when practical control is still possible.

|

NCC Expresses Reservations Over Vaccination Against HPAI

|

05/06/2024 |

|

It is becoming increasingly evident that the U.S. poultry industry is divided on the desirability of preventive vaccination against Highly Pathogenic Avian Influenza. Given the duration and severity of the H5N1 epornitic that has persisted in seasonal waves of incidence since 2022, both turkey and egg production segments have been disproportionately affected. In contrast there have been limited losses among broiler breeder and growing farms. The ongoing epornitic has resulted in depopulation of close to 90 million birds with 75 percent comprising commercial egg laying flocks or pullets, 16 percent turkeys and 7 percent broilers and broiler breeders. It is becoming increasingly evident that the U.S. poultry industry is divided on the desirability of preventive vaccination against Highly Pathogenic Avian Influenza. Given the duration and severity of the H5N1 epornitic that has persisted in seasonal waves of incidence since 2022, both turkey and egg production segments have been disproportionately affected. In contrast there have been limited losses among broiler breeder and growing farms. The ongoing epornitic has resulted in depopulation of close to 90 million birds with 75 percent comprising commercial egg laying flocks or pullets, 16 percent turkeys and 7 percent broilers and broiler breeders.

At issue is the potential impact of even limited regional and sector vaccination on the export of broiler leg quarters. The prevailing perception is that introducing any program of preventive vaccination would be an acknowledgement that the infection is endemic resulting in a number of importing nations imposing wide restrictions on importation. The reality is that HPAI is effectively regionally and seasonally endemic in the U.S. given that both migratory birds that introduce infection and now many domestic species both serve as reservoirs and disseminators of the virus. Even the most extreme levels of biosecurity are ineffective in preventing introduction of infection based on anecdotal and scientific evidence that  infection can be transmitted over short distances by the aerogenous route. Since the 2022 epornitic, the USDA-APHIS has followed an outdated and anachronistic policy of eradication. This is clearly a fallacious approach, inappropriate to a disease subject to seasonal introduction and with domestic wildlife reservoirs. infection can be transmitted over short distances by the aerogenous route. Since the 2022 epornitic, the USDA-APHIS has followed an outdated and anachronistic policy of eradication. This is clearly a fallacious approach, inappropriate to a disease subject to seasonal introduction and with domestic wildlife reservoirs.

Adaptation of H5N1 to mammals with animal-to-animal transmission is evidenced by outbreaks in farmed mink and marine mammals during 2023. The recognition that the infection is now present in the U.S. dairy industry raises concern for further changes in the H5N1 genome with the potential for the emergence of a zoonotic strain.

Given that highly pathogenic avian influenza caused by H5N1 is now a panornitic present on six continents, has changed attitudes towards preventive vaccination. The World Organization of Animal Health (WOAH) has accepted this modality as an adjunct to prevention along with biosecurity and quarantine. The important question is whether limited vaccination in the U.S. would seriously impact export of leg quarters representing 97 percent of broiler exports. Given the limited number of nations receiving U.S. exports, and the fact that many of these nations have endemic infection suggests that the restraints on exports may be overstated. It is clear that many nations have and  will continue to use avian influenza as either a protective measure for domestic industries or for political purposes. China applies vaccination against endemic HPAI but imposes prolonged restrictions on U.S. counties and states with diagnosed infections. This nation will act in their own interest irrespective of international agreements or scientific reality. Many importing nations would be willing to limit restrictions to the county level. Others might accept a certification program by which complexes or flocks of origin could be demonstrated to be free of virus by PCR assay prior to harvesting. will continue to use avian influenza as either a protective measure for domestic industries or for political purposes. China applies vaccination against endemic HPAI but imposes prolonged restrictions on U.S. counties and states with diagnosed infections. This nation will act in their own interest irrespective of international agreements or scientific reality. Many importing nations would be willing to limit restrictions to the county level. Others might accept a certification program by which complexes or flocks of origin could be demonstrated to be free of virus by PCR assay prior to harvesting.

|

The NCC is justified in continuing to quantify the effect of trade restrictions although in reality vaccination would result in probably less disruption than is currently imposed. The contention that vaccination would not eradicate HPAI is well recognized, but it must be accepted that the infection is now regionally and seasonally endemic. The statement that vaccination “masks the presence of HPAI” is valid but flocks can be certified free of infection using PCR technology.

The NCC statement that “We currently support USDA and APHIS stamping out policy to eradicate the virus is essentially fallacious and self-serving since this is an unachievable objective and reflects the thinking of the 1990s. The NCC encouragement of APHIS to “work with our trading partners to ensure that should a vaccination strategy be developed, we can continue to feed the world with poultry products” represents a departure from the ‘no-vaccination ever’ message. The NCC is justified in its reservations over HPAI vaccination with respect to export and trade since this is of vital economic importance to the industry that must market 15 percent of RTC volume in the form of leg quarters, an undifferentiated relatively low-priced commodity.

The recent article by Mike Brown, President of the NCC, in a Delmarva publication indicates a more reasoned approach to vaccination that recognizes that the infection cannot be eradicated through ongoing depopulation of flocks. Effective biosecurity (as opposed to the ‘make-belief’ version practiced) will not provide absolute protection against infection given the reality of aerogenous transmission.

Restriction on trade in poultry products as the result of vaccination may be influenced by future events including: -

- The unfortunate but likely possibility of introduction of HPAI into the U.S. broiler industry, resulting in significant losses.

- Recognition of HPAI among commercial flocks in Brazil.

- Extension of H5N1 or other strains to workers on U.S. livestock farms, processing and packing plants and their contacts.

- Availability of effective AI vaccines for mass application.

The “softening” of resistance by the broiler industry to preventive vaccination is encouraged and reflects an appreciation of the realities of the disease, the widespread distribution, financial impact and zoonotic potential. The NCC and USAPEEC should motivate the lifting of trade barriers against vaccination through representations to the WOAH, the International Poultry Council and the International Egg Commission to facilitate controlled and monitored immunization of egg-production and turkey flocks in U.S. areas of high risk.

|

USDA-APHIS Belatedly Releases Incomplete AI Virus Sequence Data

|

04/24/2024 |

|

On Sunday, April 21st, USDA-APHIS released 239 genetic sequences relating to H5N1 isolates. The data was released to the National Library of Medicine database as raw sequence data (FASTQ files). The sequences lacked essential supporting information that can be used by molecular epidemiologists to ascertain the sources of the isolates and how they have evolved over time. On Sunday, April 21st, USDA-APHIS released 239 genetic sequences relating to H5N1 isolates. The data was released to the National Library of Medicine database as raw sequence data (FASTQ files). The sequences lacked essential supporting information that can be used by molecular epidemiologists to ascertain the sources of the isolates and how they have evolved over time.

An alternative database, the Global Initiative on Sharing All Influenza Data (GISAID), was established by scientists under the guidance of the World Health Organization to monitor the emergence of both human and animal influenza strains. The objective was to identify viruses with zoonotic and pandemic potential. Information posted to GISAID contains consensus sequences that have been refined and are devoid of contamination and errors. These sequences are supported by the origin of the sample, species and the location and time of collection. The data posted by USDA identifies ‘time’ as 2024 and ‘location’ as USA.

In late 2019, scientists and regulatory officials worldwide condemned China for reluctance to release sequences and detailed information on SARS-CoV-19 and their subsequent removal of molecular biological information from data sets that they maintained. Are we not in a similar situation? Is this due to institutional ignorance since deliberate obfuscation could never be contemplated by a U.S. agency! Why was USDA-APHIS or ARS holding 239 sequences when the H5N1 HPAI epornitic has persisted since 2022? In late 2019, scientists and regulatory officials worldwide condemned China for reluctance to release sequences and detailed information on SARS-CoV-19 and their subsequent removal of molecular biological information from data sets that they maintained. Are we not in a similar situation? Is this due to institutional ignorance since deliberate obfuscation could never be contemplated by a U.S. agency! Why was USDA-APHIS or ARS holding 239 sequences when the H5N1 HPAI epornitic has persisted since 2022?

Notwithstanding the paucity of data released, molecular epidemiologists were able to draw some conclusions. Dr. Michael Worobey, at the University of Arizona, was able to determine that the most recent common ancestor of the H5N1 isolates from dairy cows was introduced into herds during mid- to late December 2023. This has profound epidemiologic implications suggesting widespread infection, notwithstanding the apparently low morbidity rate in infected herds. The larger question relates to the extent of H5N1virus in U.S. dairy herds given that asymptomatic cows have yielded positive nasal swabs. The revelation that PCR assays on commercial milk have yielded viral RNA, but not live replicating virus in 58 out of 150 samples from ten states is not unexpected and suggests widespread infection. Epidemiologists affiliated to GISAID are eager to access curated sequences to continue studies and to determine the potential for emergence of a human pandemic strain.

On the positive side, only one individual working with dairy cows who demonstrated conjunctivitis has yielded H5N1 virus, but with no evidence of human-to-human transmission. Preliminary studies confirmed that the H5N1 virus isolated from the dairy farm in Texas was similar to the virus isolated from a dairy farm in Michigan that received animals from the index case. The virus isolated from the extensive outbreak in laying hens in Michigan and implicated in a preliminary field investigation of the source of infection conformed to a common cluster. Enigmatically, the genetic sequence from the human case on the Texas dairy farm was sufficiently different from the similar wild bird, cat, cow and chicken sequences suggesting a different origin of infection. Evidently the worker did not contract infection from contact with cows on the index dairy herd in Texas. Dr. Tom Peacock, affiliated with the U.K. Pirbright Institute, noted, “The virus is basically too distant a cousin to be connected directly to the outbreak which either means it is either from a second spillover or that there was an early bifurcation of the cattle sequences.”

Susceptibility of mammals to the avian strain of H5N1 has been known since mid-2023 given isolation from scavenging mammalian species in North America including skunks, raccoons, pumas, coyotes and bears. Emergence of the infection in farmed mink in Spain and in marine mammals was clearly associated with animal-to-animal transmission.

Under the aeg is of the Pan-American Health Organization, scientists in Latin America have made available sequences from marine mammals and migratory birds. They have organized meetings to review findings and to consider contingency plans in the event of an emergence of a zoonitic strain of H5N1. is of the Pan-American Health Organization, scientists in Latin America have made available sequences from marine mammals and migratory birds. They have organized meetings to review findings and to consider contingency plans in the event of an emergence of a zoonitic strain of H5N1.

EGG-NEWS has previously criticized USDA-APHIS for their pedestrian approach to HPAI , comprising a repetitive sequence of diagnosis, depopulation and decontamination. Failure to assign adequate resources to field and molecular biology and an apparent reluctance to aggressively investigate and publish on the epidemiology of avian influenza represents a grievous and ultimately costly omission. The egg-production and turkey segments of the poultry industry have experienced an ongoing epornitic extending over two years and involving depopulation of over 70 million commercial birds. This has been costly to the public sector, to producers and ultimately consumers.

This criticism is now extended to a lack of transparency with respect to releases on the molecular epidemiology of HPAI and publication of annotated sequences. Dr. Rick Bright who led the Biomedical Advance Research and Development Authority from 2016 to 2020 stated, “It’s so critical that the U.S. Government should be as transparent as they can right now and share sequences and all of the data so the world can look at it and make their own risk assessment and start making their own vaccines if they need to.” Bright continued, “What would we say if this particular virus did get out of control? Would we look back on these last two or three months and say I wish we would have done something else? We must share all these sequences so the world can get ready.” This criticism is now extended to a lack of transparency with respect to releases on the molecular epidemiology of HPAI and publication of annotated sequences. Dr. Rick Bright who led the Biomedical Advance Research and Development Authority from 2016 to 2020 stated, “It’s so critical that the U.S. Government should be as transparent as they can right now and share sequences and all of the data so the world can look at it and make their own risk assessment and start making their own vaccines if they need to.” Bright continued, “What would we say if this particular virus did get out of control? Would we look back on these last two or three months and say I wish we would have done something else? We must share all these sequences so the world can get ready.”

Dr. Worobey noted, “There is a whole community of colleagues around the world who have a lot of experience with influenza and often can see things or conduct analyses that might show something that others have missed.” In the unfortunate event that a zoonotic strain emerges from the current circulating H5N1 in free-living avian and mammalian species or in commercial flocks and herds, administrators at USDA-APHIS will have a lot on their collective conscience. This is attributed to their unconscionable lack of transparency and their inactivity in failing to aggressively investigate the epidemiology of HPAI. The U.S. poultry and dairy industries, consumers, and ultimately taxpayers deserve better.

|

Rising Energy Costs to Offset Trend in Deflation?

|

04/23/2024 |

|

Following eleven successive increases in the 10-year benchmark interest rate the FOMC engineered a reduction in U.S. inflation as measured by the Consumer Price Index (CPI) from 8.9 percent in June 2022 to 3.5 percent in March 2024. The increase in the benchmark interest rate did not result in unemployment and many influential economists predict a “soft landing”. Following eleven successive increases in the 10-year benchmark interest rate the FOMC engineered a reduction in U.S. inflation as measured by the Consumer Price Index (CPI) from 8.9 percent in June 2022 to 3.5 percent in March 2024. The increase in the benchmark interest rate did not result in unemployment and many influential economists predict a “soft landing”.

Despite the substantial increase in the inflation rate, attaining an elusive FOMC inflation target of approximately 2.0 percent will be difficult to accomplish. At the beginning of year, the market anticipated as many as six reductions in interest rates. The five consecutive pauses suggested caution and based on CPI, wage and employment data there will probably be only one or two reductions of 0.25 percent each in 2024 and not before late summer. Federal Reserve Chairman Powell, supported by Federal Reserve Governors, has stated in Congressional testimony and in public statements that decisions on reducing interest rates would be based on data with demonstrable progress in reducing inflation.

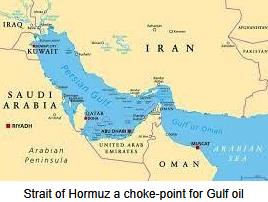

Energy is a major contributor to “sticky” inflation having increased by close to 25 percent since December 2023. Although turbulence in the Middle East could have been a significant factor in the increase, effectively disciplined restriction in output by OPEC+ has maintained price above $80 per barrel. As noted in successive weekly Economy, Energy and Commodity Reports in EGG-NEWS, the November reduction in OPEC+ output of 2.2 million barrels a day was extended through June representing two percent of global production. Non-OPEC output including Brazil, Angola and the U.S. has in large measure moderated the effect of the OPEC+ constraints. OPEC+ has learned that high oil prices reduce demand, and the Cartel has acquired the skill and discipline to fine-tune supply to regulate price and to disfavor alternative sources of energy.

Restoration of the economies of the E.U. and China, concurrent with increased industrial activity, will however create further demand for crude and other forms of non-renewable energy with valid predictions of a rise in price. Despite the reciprocal mutual attacks by Israel and Iran during the current month, the Brent Crude benchmark is still below $90 per barrel compared to a high of $95 in August 2023 and a recent low of $75 per barrel during November 2023. Economists predict that if OPEC cuts hold, Brent Crude could reach $100 per barrel by mid-summer attributed to increased demand.

Unknowns relating to future oil supply and prices will be influenced by possible reaction by Iran. Obviously increased sanctions against the regime will evoke a response either by the rulers of that nation or their surrogates. Interdicting transport of crude through the straits of Hormuz or additional action by Houthi rebels in the Bab-el-Mandeb strait could drive oil above $100 per barrel. This would result in international action including pressure by China, the major purchaser of Iranian oil. Given recent history, it is anticipated that Brent Crude will fluctuate between $85 and $90 per barrel though summer. Availability of domestic supply in the U.S. will probably constrain WTI crude at between $82 and $87 per barrel but higher prices will favor increased exports.

Since the price of oil is closely correlated with corn and other agricultural commodities, any escalation in price has implications for livestock production. Higher prices for diesel and gasoline will limit consumer spending with a negative effect on the earnings of food producers, distributors and retailers. According to the American Automobile Association

U.S. consumers paid on average, $3.66 per gallon for regular grade during mid-April.

It is axiomatic that the pump price of gasoline will influence the November election with high prices attributed to the incumbent party, irrespective of justification.

|

PEAK 2024 an Outstanding Success

|

04/16/2024 |

|

PEAK 2024 organized by the Midwest Poultry Federation is now well established in the Minneapolis Convention Center that provides more exhibition space, meeting rooms and hotel accommodation that the previous St. Paul location. The trade exhibition consistently attracts more egg-related allied suppliers compared to the IPPE. The concurrent industry association meetings and educational programs are focused on egg production given the concentration of farming operations in six Midwest states. Although space limits the display of large displays including 700-case per hour graders and a range of aviary equipment, technical personnel are available on booths to discuss operational parameters supplemented by videos, models, components and short cross-sections of installations. PEAK 2024 organized by the Midwest Poultry Federation is now well established in the Minneapolis Convention Center that provides more exhibition space, meeting rooms and hotel accommodation that the previous St. Paul location. The trade exhibition consistently attracts more egg-related allied suppliers compared to the IPPE. The concurrent industry association meetings and educational programs are focused on egg production given the concentration of farming operations in six Midwest states. Although space limits the display of large displays including 700-case per hour graders and a range of aviary equipment, technical personnel are available on booths to discuss operational parameters supplemented by videos, models, components and short cross-sections of installations.

Educational programs presented included the North Central Avian Disease Conference, the Organic Egg Farmers of America Symposium, the Devenish Nutrition Symposium, and a number of informal gatherings taking advantage of attendance at the event. Educational programs presented included the North Central Avian Disease Conference, the Organic Egg Farmers of America Symposium, the Devenish Nutrition Symposium, and a number of informal gatherings taking advantage of attendance at the event.

The Midwest Poultry Federation arranged a series of educational presentations for pullet and egg management, feed technology and business leadership. During the trade exhibition, poultry TED Talks were presented detailing innovations in products and management for the benefit of attendees. Entertainment included PEAK Unhatched, an Exhibition-floor Happy Hour and Hospitality Night.

Despite the prevailing favorable margins in egg production, there were a number of overhangs that detracted from optimism:

- The resurgence of highly pathogenic avian influenza with three complexes affected since the beginning of April requiring depopulation of close to six million hens in two states was the major issue of concern. It is evident that HPAI is no longer limited to seasonal epornitics but has expanded beyond the migration of waterfowl in spring and fall months. This is in all probability due to transfer of the H5N1 virus to non-migratory species of free-living birds. This is evidenced by dead grackles and pigeons yielding H5N1 virus in the vicinity of the index dairy farm in Texas that was affected with Bovine Influenza-H5N1. Outbreaks of HPAI have been regularly diagnosed on a weekly basis in backyard flocks in diverse states outside the migratory seasons. These small flocks serve as sentinels for the presence of avian influenza virus and many cases are not diagnosed. Sometime in 2024 the USDA-APHIS will have to accept regional vaccination for turkeys and egg-production flocks. It must be obvious by now that it is futile to attempt to eradicate an endemic infection spread by the aerosol route in addition to fomites.

- The impasse in Congress is impeding passage of legislation necessary to maintain agricultural production. The Farm Bill is mired in dissent in both the Senate and House Agricultural Committees with polarization separating left and right-leaning members. Ultimately there will have to be compromise on the two issues of contention represented by allocations for SNAP and WIC favored by the left and diversion of funds from climate change programs to commodity price support on the right. The 118th Congress has barely passed fifty bills as opposed to an anticipated 400 in a normal two-year period. Appropriations bills were delayed by months by resorting to stop-gap continuing resolutions. Both parties are to blame for their lack of commitment to the national interest caused by grandstanding and intra-party conflict.

- There was considerable talk in the hallways at PEAK of consolidation in the retail food sector. The proposed merger between the Kroger Company and Albertsons Corporation is a concerning issue since this would create more buying power for the chains that are readily able to adjust orders to influence the industry benchmark price discovery system to the disadvantage of producers.

- There are concerns over the economy. The Federal Reserve has obviously reduced inflation from 8.9 to 3.5 percent but is experiencing difficulty in reducing levels to the target of 2.0 percent. International conflict and the price of energy are adding to the burden of inflation that is reducing consumer spending despite the last hurrah of extravagance during the first quarter of 2024.

- As in all planting seasons, there is concern over the anticipated crop. With the projected cyclic transition from a La Nina to an El Nino event, weather patterns during the 2024 growing season will influence yields. Lower feed prices have contributed to positive margins over the past twelve months but an unfortunate combination of higher input costs with production exceeding demand may impact profitability in the late third and early fourth quarters.

It is hoped that the contributions derived from PEAK 2024 in the form of technical and trade information will be transferred from the event to all U.S. production units and companies with evident improvements in productivity and profitability.

|

Relative Cost of Groceries

|

04/04/2024 |

|

Dr. Leo Feler, Chief Economist at Numerator, recently published on prices of groceries and their affordability. During January 2020, that marked the beginning of the COVID years, through December 2023, the cost of at-home food rose by an average of 25 percent. Income, however, increased 24 percent over the same period, offsetting the average rise in shelf prices. Dr. Leo Feler, Chief Economist at Numerator, recently published on prices of groceries and their affordability. During January 2020, that marked the beginning of the COVID years, through December 2023, the cost of at-home food rose by an average of 25 percent. Income, however, increased 24 percent over the same period, offsetting the average rise in shelf prices.

Dr. Feler documented an increase in price for food categories over the four-year period with poultry, fish and eggs increasing at 26 percent and the lowest category, dairy and related products, at 21 percent. His predictions are for stability in price going forward with low, single-digit increases paralleling the situation before COVID that resulted in difficulties in the supply chain.

Despite the economic reality that grocery items are as affordable now as they were in 2020, there is a perception that prices are higher. This is evidenced by recent comments from the White House relating to “price gouging” and “shrinkflation” and echoed in statements by the Federal Trade Commission.

Consumers have adapted to higher prices by searching for value, hence, the rise in popularity of house brands. Surveys showed that forty percent of consumers are buying more private brands and reducing expenditure on unnecessary food items. They are also buying in bulk as reflected in the reported revenue of Costco, Sam’s Club and B.J.’s. Consumers are also calculating cost per unit and splitting their grocery purchases among competing stores to take advantage of special offers.

According to Steve Markenson, Vice-President of Research at the Food Marketing Institute, consumers are now considering convenience and quality in addition to cost in evaluating items. The deep discounters, led by Aldi, have obviously benefited through low operating costs, limited range of SKUs and demonstrably lower prices based on their private ownership and business model.

It is evident that retailers that can negotiate favorable prices from their suppliers contributes to higher gross margins and improvement in the bottom line. This only benefits consumers if there is a pass-through of savings. The check-out point and the print-out of the transaction either reinforces or dispels the perception of value.

Dr. Leo Feler, Chief Economist, Numerator Inc. |

Given the increase in eat-at-home, and with increased concern over the price of groceries, promotion of eggs should emphasize value. This includes an emphasis on nutrient content against alternatives including dairy, red meat and plant-based alternatives. Since the expanded concept of value incorporates convenience and ease of preparation, the American Egg Board should address the inherent attributes of eggs and develop a “not just for breakfast” message. Food manufacturers should be encouraged to incorporate egg-derived products in foods and develop a range of snacks and meal presentations featuring eggs as a source of high-quality protein with limited caloric contribution to diets.

|

Scientific Realities Should Moderate Official Statements on Avian and Bovine Influenza

|

04/04/2024 |

|

To date, APHIS has been factual in their minimal reporting on the ascending incidence of bovine influenza-H5N1. In contrast, a number of State Veterinarians have been far more optimistic in their official statements dampening concern over the potential of the virus to become zoonotic. To date, APHIS has been factual in their minimal reporting on the ascending incidence of bovine influenza-H5N1. In contrast, a number of State Veterinarians have been far more optimistic in their official statements dampening concern over the potential of the virus to become zoonotic.

The major concern is the possible emergence of a zoonotic strain of H5N1 as noted by the World Health Organization that regards the virus as a potentially pandemic strain requiring surveillance over a range of avian and mammalian species. At this time, there is no evidence that spontaneously altered strains of H5N1 are infectious to humans although affecting a wide range of terrestrial and marine species with evident animal-to-animal spread. Despite the recovery of H5N1 virus from a dairy-herd employee with conjunctivitis, the only previous U.S. case occurred in a worker involved in depopulation of an infected flock. Given thousands of worker hours of exposure in 2015 and then again during the 2022-2023 epornitics, one asymptomatic case suggests that even with extreme exposure, humans are currently refractory to infection. The major concern is the possible emergence of a zoonotic strain of H5N1 as noted by the World Health Organization that regards the virus as a potentially pandemic strain requiring surveillance over a range of avian and mammalian species. At this time, there is no evidence that spontaneously altered strains of H5N1 are infectious to humans although affecting a wide range of terrestrial and marine species with evident animal-to-animal spread. Despite the recovery of H5N1 virus from a dairy-herd employee with conjunctivitis, the only previous U.S. case occurred in a worker involved in depopulation of an infected flock. Given thousands of worker hours of exposure in 2015 and then again during the 2022-2023 epornitics, one asymptomatic case suggests that even with extreme exposure, humans are currently refractory to infection.

Although there have been over 800 documented cases of H5N1 or H7N9 influenza among humans in Asia over two decades, the attack rate is exceptionally low given the level of potential exposure since emergence of these strains in poultry. Most of the cases involved either the elderly or the immunosuppressed. Patients in most instances presented with a history of contact with live poultry either on farms or in wet markets as with the two cases documented in South America in 2023.

Given the reality that migratory marine birds and waterfowl are susceptible to H5N1 and disseminate the virus across five continents, ultimately, mutations may occur that may result in a zoonotic strain. The higher the concentration of susceptible birds or livestock in an area or on a farm, the greater will be the probability of either a mutation or a recombinant event.

Accordingly, it would be advisable to consider human health as a justification to create non-susceptible commercial bird populations through immunization. Currently, archaic and inappropriate trade restrictions in addition to the imposition of contrived trade barriers disfavor universal adoption of vaccination. The World Organization of Animal Health supports the principle of vaccination and clearly states that this modality should not be a restraint to trade providing there is adequate surveillance to detect infection in immunized flocks. In the age of PCR, this is an achievable objective. It will be possible for regulator y authorities to introduce and manage a program of certification to confirm that export consignments are derived from flocks free of infection. y authorities to introduce and manage a program of certification to confirm that export consignments are derived from flocks free of infection.

The concerns of the broiler segment of the U.S. poultry industry concerning vaccination are recognized. When human health is considered, the potential of losing export sales pales in significance to even the slightest risk of an emerging pandemic. The cost of COVID with the attendant loss of more than one million of our fellow citizens suggests that H5N1 avian influenza is more than just a “chicken and turkey problem”.

It is now time to implement regional vaccination against HPAI in areas with a history of infection and specifically for turkey and egg-production flocks. The associations representing the segments of the U.S. poultry industry, APHIS, USAPEEC and the Office of the U.S. Trade Representative need to coordinate and intensify their activities to accept rigorously controlled vaccination. As far as possible, issues relating to restraint in trade based on vaccination should be resolved given that HPAI is now panornitic in distribution.

A statement by a mid-west State Veterinarians that “research to date has shown that mammals appear to be dead-end hosts which means that they are unlikely to spread HPAI further” is simplistic and is devoid of substantiation by either current virology or epidemiology. State Veterinarians are tasked with preserving the health of flocks and herds under their jurisdiction and should not be cheer-leaders for consumption of livestock products. With respect to HPAI, there is more at risk than either loss of trade or the cost of depopulation. Creating a solidly immune population of commercial poultry would contribute to a lower risk of facilitating a zoonotic strain of avian influenza. The emergence of bovine influenza-H5N1 in March and outbreaks in mink and marine mammals should be a warning of the potential for an influenza pandemic reminiscent of the 1918-1919 catastrophe. Risks of mutation might be small but economic and humanitarian consequences are infinite.

|

FTC Report Implicates Large Grocery Chains in Food Inflation

|

03/25/2024 |

|

A March 21st report issued by the Federal Trade Commission (FTC) identified the involvement of major retail grocery chains in food inflation following supply chain disruptions coincident with the COVID years. The report analyzed the actions of producers, wholesalers and retailers in “skyrocketing prices for groceries” that impacted consumers. A March 21st report issued by the Federal Trade Commission (FTC) identified the involvement of major retail grocery chains in food inflation following supply chain disruptions coincident with the COVID years. The report analyzed the actions of producers, wholesalers and retailers in “skyrocketing prices for groceries” that impacted consumers.

The report demonstrated that larger chains benefitted at the expense of smaller competitors. The focus of the report included Walmart, Amazon, Kroger, C&S Wholesale Grocers, Proctor and Gamble, Tyson Foods, Kraft-Heinz and Associated Wholesale Grocers Inc. The FTC report demonstrated the power of major retailers and their impact on the supply chain based on buying power to the disadvantage of smaller, regional grocery chains.

The FTC report documented that large retailers increased their revenue by more than six percent in relation to costs during 2021 through 2023 without commensurate increases in operating expenses. The report also documented pressure on suppliers relating to prices and delivery. The FTC report documented that large retailers increased their revenue by more than six percent in relation to costs during 2021 through 2023 without commensurate increases in operating expenses. The report also documented pressure on suppliers relating to prices and delivery.

The report was welcomed by the National Grocers Association (NGA), representing independent and small stores. Chris Jones, the Chief Government Relations Officer for the NGA, noted the past failure of the FTC and DOJ to use existing legislation to suppress pricing decisions that disfavor consumers and small suppliers. The NGA president, Greg Ferrara, stated, “Decades of lax antitrust enforcement enables grocery buyers to coercively squeeze suppliers to comply with their trade demands, unfairly disadvantaging smaller competitors”.

The Robinson-Patman Act specifically disallows both discriminatory and predatory pricing. Buyers who benefit from these practices violate the Act if the buyer pressures producers to agree to lower prices for commodities of similar grade and quality. This would apply specifically to generic USDA graded eggs that are a commodity in interstate commerce.

The FTC report coincides with a lawsuit intended to block the merger of the Kroger Company with Albertsons Corporation. The Administration recognizes the political benefits of consumer protection in a pre-election year. Notwithstanding the intensified enthusiasm for anti-corporate action, it must be recognized that egg producers have been nickeled and dimed by the major chains over decades. This has reduced margins and deprived producers of sufficient profit to re-invest in maintenance and expansion. An added burden with less than adequate reimbursement is represented by the need to convert housing from conventional cages to alternative systems since 2020 to comply with welfare requirements. The FTC report coincides with a lawsuit intended to block the merger of the Kroger Company with Albertsons Corporation. The Administration recognizes the political benefits of consumer protection in a pre-election year. Notwithstanding the intensified enthusiasm for anti-corporate action, it must be recognized that egg producers have been nickeled and dimed by the major chains over decades. This has reduced margins and deprived producers of sufficient profit to re-invest in maintenance and expansion. An added burden with less than adequate reimbursement is represented by the need to convert housing from conventional cages to alternative systems since 2020 to comply with welfare requirements.

The situation in the U.K. parallels the findings of the FTC with regard to pressure on producers. As with the U.S retail grocery in the U.K. is an oligopoly with a few retailers sourcing domestic-produced and some imported shell eggs. After Brexit feed and energy costs soared but retailers failed to adjust prices to allow independent producers of free-range eggs, comprising half of national supply, to reach break-even. The result was a sharp decline in availability as producers ceased operation due to exhausting working capital and credit. Eventually many of the large chains were obliged to make ex gratia payments to individual producers to restock housing and to resume production.

The wholesale price of packed generic eggs in the U.S. should be subject to the law of supply and demand. Cyclic periods of oversupply that were a feature of the 1980s through the 2010s have given way to a more rational rate of expansion following consolidation, conversion to non-caged housing and more reliable market intelligence. Unfortunately the prevailing industry benchmark reporting service now appears to function to the detriment of producers. The daily quotations appear to amplify downward movement in price and allows chain buyers the opportunity to depress prices over the short term by temporarily withholding orders. This results in a disproportionately low price, exacerbating price elasticity. A Midwest-large Chicago Mercantile Exchange (CME) quotation would be more equitable given that the costs of corn and soybean meal representing 65 percent of nest run expense is determined by the CME. The wholesale price of packed generic eggs in the U.S. should be subject to the law of supply and demand. Cyclic periods of oversupply that were a feature of the 1980s through the 2010s have given way to a more rational rate of expansion following consolidation, conversion to non-caged housing and more reliable market intelligence. Unfortunately the prevailing industry benchmark reporting service now appears to function to the detriment of producers. The daily quotations appear to amplify downward movement in price and allows chain buyers the opportunity to depress prices over the short term by temporarily withholding orders. This results in a disproportionately low price, exacerbating price elasticity. A Midwest-large Chicago Mercantile Exchange (CME) quotation would be more equitable given that the costs of corn and soybean meal representing 65 percent of nest run expense is determined by the CME.

Examination of pricing policies of large grocery chains by the FTC is long overdue and was in all probability a byproduct of the investigation of the proposed Kroger merger (or acquisition) with Albertsons. This transaction would be detrimental to suppliers, workers and consumers as evidenced by lawsuits filed by the Attorneys General of eight states and the FTC.

|

U.S. Economy Currently Strong – But Will it Last?

|

03/19/2024 |

|

It is axiomatic that a strong U.S. economy is beneficial for the poultry industry. Availability of capital allows for investment in expansion and installation of equipment that promotes efficiency. Increased spending power encourages consumption reflected in higher demand and margins. At the end of the first quarter of 2024, the U.S. economy is strong but is vulnerable to inappropriate fiscal policy and political pressures. Over the past five years, the U.S. economy has grown eight percent in real terms compared to the E.U. at three percent, Japan at one percent and negative growth among other nations.

Despite successive rate increases as determined by the Federal Reserve FOMC, unemployment has remained at an exceptionally low level, currently 3.9 percent and the economy is moving towards a “soft landing”. Economists suggest that despite proving “sticky” inflation should decline to approximately 2.2 percent on an annual basis by the end of 2024 with a concurrent forecast of a 3.2 percent growth in GDP. This, in large measure, has been achieved through increased productivity with a 2.6 percent increase in the non-farm categories and 0.6 percent overall.

The U.S. achieved the current, favorable position through injection of capital during the immediate post-COVID years. This largesse was accompanied by an average deficit of 14 percent of GDP in 2020 and 2021 compared to less than half this level among Euro nations. Other factors contributing to a favorable situation include energy independence and the relatively low cost of the range of fuels used compared to the E.U. The labor force has increased to approximately 160 million workers, up four percent from 2019. This has been driven by immigration with the foreign-born component up by 16 percent since the advent of COVID. Despite immigration, unemployment is at a low level under 4 percent with 10 million positions open albeit with moderate wage increases.

Despite the current favorable situation, there are certainly clouds on the horizon. Stimulation of the economy through government spending is widening the national deficit. In 2022, the deficit was 4.0 percent of GDP but rose to 7.5 percent in 2023. The nation is now spending as much on annual interest as it does on defense. One concern is the high proportion of debt held by China that is experiencing a decline in their economic growth and the holdings by other “unfriendly” nations. Problem areas include delinquency on credit cards suggesting that consumer spending, a major driver of the economy, will falter. This is despite the fact that high-income consumers representing 20 percent of earners are responsible for 45 percent of consumption. It is inevitable that this demographic will tighten their purse strings. Restrictive climate-related legislation is imposing costs on the economy. As an example the U.S. is currently the world's largest supplier of LNG. Executive orders limiting expansion of export terminals will be detrimental to reversing the foreign trade deficit. The property market appears vulnerable to sustained high interest rates and post-COVID factors including work-from-home have reduced occupancy rates for commercial property that cannot be converted to housing to provide an equivalent return. This may reflect on the stability of regional banks that are vulnerable to now questionable security and the performance of their loan portfolios.

Of greatest concern will be the policies implemented by the eventual winner of the 2024 Presidential election. The opposing candidate is expressing views that promise extreme protectionism with high tariffs. This would be detrimental to the economy. Concurrently an anti-immigration bias would deprive U.S. industry of necessary workers. Interference in the independence of the Federal Reserve would also be detrimental to the standing of the U.S. as evidenced by the economies of nations such as Turkey where injudicious political pressure over interest rates has proven disastrous to the value of the Nation’s currency. Promises to lower taxes if they eventuate will markedly reduce revenue and widen the national debt as has occurred under the present and previous Administrations.

The incumbent candidate is promising to raise taxes on corporate earnings and on high-income earners who are the most innovative and productive. In many respects the programs to be implemented are also protectionist although it is questioned as to whether pronouncements during the 2024 State of the Union address were political rhetoric or a firm intention of policy during a second term. The proposed program of spending would intensify the magnitude of the national debt. Attempts to reverse climate change would have profound impacts on the energy industry, vital to the economy. Injudicious spending on social programs will add to the national debt especially if “investment” is not realized over the short or even intermediate term.

Policies and programs implemented by the USDA in recent years using funding from the CARE Act that are intended to encourage local production and assist the “disadvantaged and under-represented” may not even contribute to intermediate-term productivity. Attempts to restructure the meat industry are quixotic and contrary to the realities of economies of scale and efficiency. From the perspective of providing inexpensive protein, oligopolies should be tolerated with appropriate protection for farmers, given the needs to supply the domestic and export markets, some of which are eroding.

Despite the favorable economic situation as quantified each week in the EGG-NEWS Economy, Energy and Commodity Report, some changes will be necessary to ensure a “soft landing” as anticipated. Both candidates for the Presidency should now moderate their rhetoric and adopt acceptable and productive economic policies based on sound economic principles. The Federal Reserve should address the issue of the delay in reducing interest rates given the trajectory in the decline in inflation to three percent. It is noted that eleven previous cycles of suppressing inflation by increasing interest rates, the economy entered into recession ten times. A repetition could be averted by three rate cuts from June onwards. Currently, the economy is in good hands. Let us hope prudence and sound judgment resist the temptation to impose isolationism or to continue with intemperate government spending, throttling the energy industry and failing to introduce a rational program of immigration. Hopefully, politicians and economists will see common ground and continue to guide the progress of our Nation for the benefit of both producers and consumers.

|

Corporate Greed and Shrinkflation Emerging as Unjust Election Issues

|

03/12/2024 |

|

Despite the fact that inflation is receding, there is both perception and reality that the prices of food items have not declined in proportion to other items. Deflation has, in large measure, been a reflection of the lower cost of energy although it is generally accepted that a gas price above $3.25 impact budgets and influences voters more than fluctuation in the price of a dozen eggs or a pound of ground beef. In actuality inflation as measured by the Consumer Price Index has declined from 8.9 percent in June 2022 to 3.2 percent in February 2024.

It is apparent that the Presidential re-election campaign will involve messages implying that the food manufacturing and distribution sectors are indulging in “corporate greed” and that prices are unnecessarily high and that unscrupulous companies are employing shrinkflation for packaged goods. This was emphasized in the 2024 State of the Union address and according to polling, resonates with the electorate.

Inflation was an inevitable result of injecting trillions of dollars into the economy in response to the emergence of COVID with widespread disruption of production capacity and consumption. Economists including ex-Treasury Secretary, Larry Sumner warned of the effect of inflation, but this was to be a price to pay to avoid a depression. We did not have soup and breadlines on Wall street or Hoovervilles on the Mall but we still have homelessness and SNAP. Through skill and a measure of luck, the Federal Reserve has guided the economy over the past three years to what is forecast to be a “soft landing” without resulting in mass unemployment. Compared with other industrialized nations, the U.S. has emerged from the pandemic with a relatively strong economy as measured by gross domestic product, with Q4 GDP at 3.2 percent, low unemployment of 3.9 percent in February 2024 and increasing agricultural and industrial productivity.

The Administration message that the food production sector is taking advantage of consumers is incorrect and unjustified. While there may be isolated cases of overt shrinkflation or price gouging, profit margins generated by food producers are consistent with restraint in pricing that is expected in a free market and competitive economy.

Political rhetoric conveniently forgets the twenty percent increase in wage rates over the past five years. This is reflected in all components of the food production chain from field workers through to serving. Quoted in Politico, Dean Baker a Senior Economist at the right leaning Center for Economic and Political Research, stated, “We are not going to have a world where people get to keep their 20 percent pay increases and pay what they did four years ago for food. Political rhetoric conveniently forgets the twenty percent increase in wage rates over the past five years. This is reflected in all components of the food production chain from field workers through to serving. Quoted in Politico, Dean Baker a Senior Economist at the right leaning Center for Economic and Political Research, stated, “We are not going to have a world where people get to keep their 20 percent pay increases and pay what they did four years ago for food.

The largesse exhibited during the COVID period comprising Federal funding through the Coronavirus Aid, Relief in Economic Security (CARES) Act of 2020 and the American Rescue Plan of 2021 in all probability averted a depression. Not even the U.S. government can realistically spend the artificial money created. Various Departments including the USDA still hold undistributed funds that should be returned to the Treasury to offset the national debt. Funds made available to the Department of Agriculture have been misused in futile attempts by Secretary Tom Vilsack to restructure protein production. He has consistently attempted to oppose the major packers and broiler integrators through new regulations under the Packers and Stockyards Act. He has distributed vast sums to unproductive projects claiming support for the “disadvantaged and underrepresented” in agriculture. The scale of USDA “giveaways” has intensified this year possibly because administrators and initiators of programs recognize the likelihood of a change in administration that would bring about an end to their activities.

Inverse relationship between ascending Fed rate and deflation |

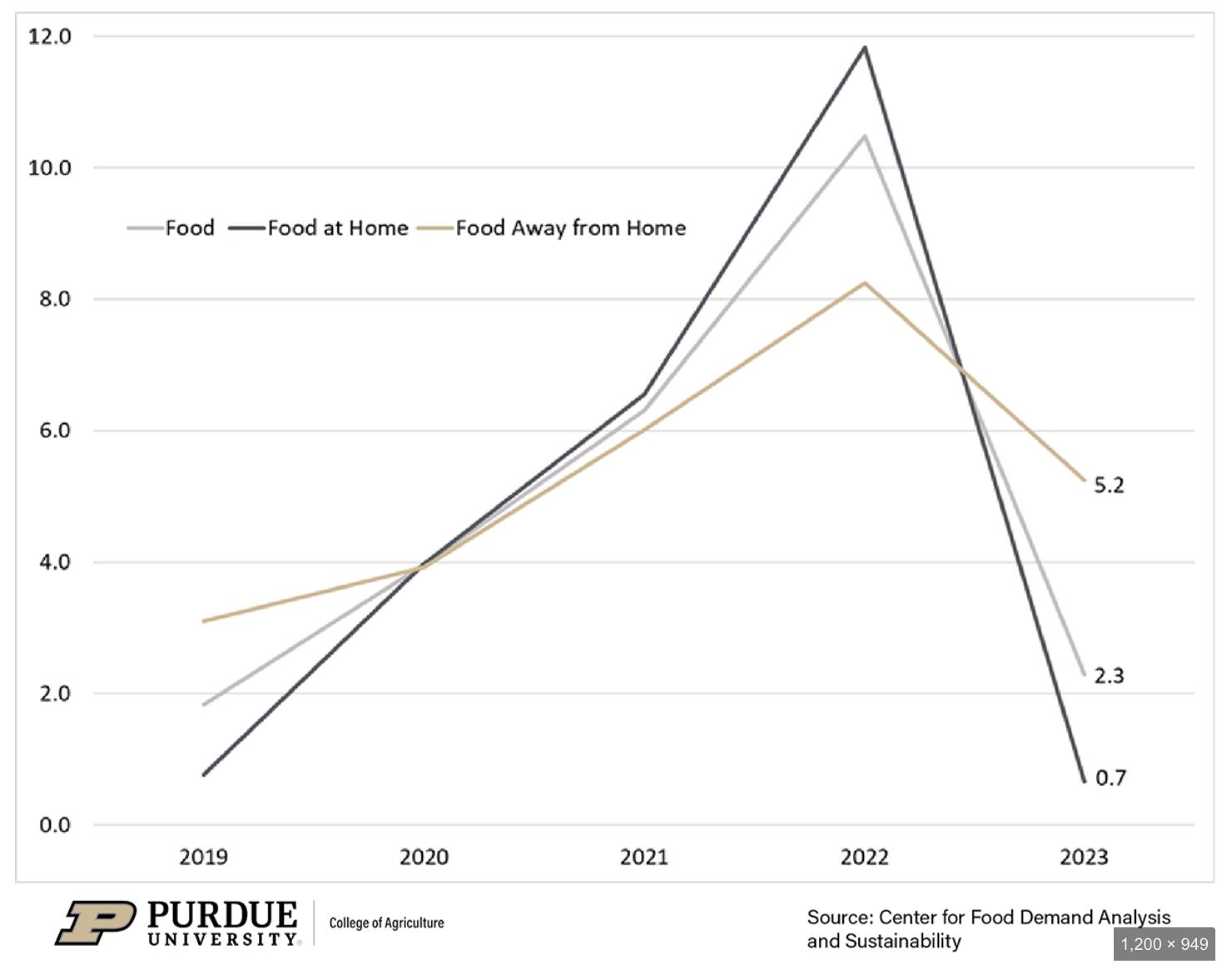

It is unfortunate that the agricultural sector and the food industry have become targets of political rhetoric through unjust accusations of corporate greed. The Administration has attempted to divert criticism from current disaffection to focus on an essentially innocent industry. This is confirmed in the March 12th release of the Consumer Price Index that documented a 2.2 percent increase in all food on an annual basis with food-at-home up 1.0 percent and food-away-from-home up 4.5 percent, reflecting labor costs.

Given that alleged price gouging and corporate greed will be emphasized as talking points in the coming election campaign, industry associations should prepare rebuttals and be able to counter unjust accusations, applying sound reasoning supported by economic facts.

Subscribers are directed to the Economy Section of the weekly Economy, Energy and Commodity Report in this edition.

|

U.S. Agriculture Needs a Workable Immigration Law

|

03/07/2024 |

|

With the apparent failure of the Immigration Bill previously agreed to in principle by both chambers of Congress, the U.S. will continue to function with legislation passed in 1990. Although agricultural workers can enter the U.S. on H-2A visas, there is a general agreement among many sectors of agriculture including dairy, produce and fruit that the allocation is inadequate. Foreign workers can be legally employed providing they comply with E-Verify requirements. There is evidence that the system of verification is being gamed with both deceptive documentation and widespread overlooking of the requirement. With the apparent failure of the Immigration Bill previously agreed to in principle by both chambers of Congress, the U.S. will continue to function with legislation passed in 1990. Although agricultural workers can enter the U.S. on H-2A visas, there is a general agreement among many sectors of agriculture including dairy, produce and fruit that the allocation is inadequate. Foreign workers can be legally employed providing they comply with E-Verify requirements. There is evidence that the system of verification is being gamed with both deceptive documentation and widespread overlooking of the requirement.

It has become politically expedient for some state administrations to pass legislation enforcing E-Verify. Florida enacted SB1718 that impacts approximately 750,000 undocumented immigrants working in the state, mainly in agriculture but also construction and tourism. What initially appeared to be a popular but discriminatory law has now emerged as a restrictive measure notwithstanding the reliance of Florida and other states on foreign labor. Both farming and business communities are experiencing difficulty in recruiting and retaining workers many of whom are undocumented. The law mandating E-Verify resulted in an exodus of workers from the state fearing deportation. SB1718 also serves as a license to exploit through wage theft, harassment and substandard accommodation given that workers are captive under illegal employment and have no legal recourse.

Attempts to enforce E-Verify in Florida resulted in protests from agricultural associations and the state Chamber of Commerce with a movement to have SB1718 rescinded given the negative economic impact. Some states including North Carolina have enacted loopholes exempting agriculture and specified industries from nominal compliance with E-Verify. Studies on the effect of enforcing E-Verify suggest profound economic loss as in Georgia in 2011 when undocumented workers left the state, resulting in a decline in agricultural revenue exceeding $100 million.

Politicians endorsing E-Verify point to the need to preserve jobs for U.S. citizens. If there were sufficient applicants from our under- and unemployed residents for available but relatively low-paid agricultural and construction positions in Florida, California and the Carolinas, there would not be a demand for foreign workers. It is questioned why the U.S. expends public funds on SNAP and unemployment benefits when jobs are available.

It is clear that the current look-the-other way approach to E-Verify favors agriculture, construction and tourism. There is a ready supply of both illegal and documented workers willing to labor for statutory minimum or sub-minimum wages. If foreign workers were not available, wage rates would rise possibly attracting unemployed U.S. workers. At some point, there will have to be a balance between legal entry with work offered at minimum wage rates coupled with employment of U.S. citizens. It is clear that the current look-the-other way approach to E-Verify favors agriculture, construction and tourism. There is a ready supply of both illegal and documented workers willing to labor for statutory minimum or sub-minimum wages. If foreign workers were not available, wage rates would rise possibly attracting unemployed U.S. workers. At some point, there will have to be a balance between legal entry with work offered at minimum wage rates coupled with employment of U.S. citizens.

E-Verify currently is subject to inaccuracies that place eligible workers at a disadvantage and allows fraudulent credentials. Perhaps if the E-Verify system were to be modified, to become reliable and accurate and if it would become the law of the land, with an adequate supply of H-2A visas, the labor situation might be improved.

Inclusion of a pathway to permanent residency and eventually citizenship, as offered by Canada, was a major objection to the proposed Immigration Bill that has been under review since 2019. An E-Verify federal mandate should be included in a comprehensive immigration bill but with adequate availability of H-2A visas. Farmers and companies that rely on and benefit from foreign labor would be more productive and profitable. A just and equitable immigration bill specifying the rights and obligations of foreign workers and employers would benefit the economy and all concerned.

|

USDA Edging Inexorably Towards AI Vaccination

|

02/19/2024 |

|

In a statement issued on February 14th, Secretary of Agriculture Tom Vilsack stated, “The USDA is 18 months or so away from identifying a vaccine for the current strain of bird flu and is developing a process to distribute it.” This Orwellian “officialspeak” was also entered into testimony before a Congressional hearing. In a statement issued on February 14th, Secretary of Agriculture Tom Vilsack stated, “The USDA is 18 months or so away from identifying a vaccine for the current strain of bird flu and is developing a process to distribute it.” This Orwellian “officialspeak” was also entered into testimony before a Congressional hearing.

For the record:

- The current H5N1 strain of avian influenza, is essentially a pandemic strain prevalent North and South America, Asia, Africa, and Europe for over three years. The strain is responsible for losses of over 100 million commercial poultry and has made severe inroads into the populations of susceptible marine and migratory birds.

- Vaccines are available off-the-shelf. The major multinational biopharmaceutical manufacturers could, subject to authorization and in the absence of bureaucratic restraints supply the needs of the U.S. poultry industry within weeks. There would be sufficient vaccine to implement regional vaccination programs for required egg production flocks, turkeys, and broiler breeders in areas at risk.

- The USDA does not have to “develop a process to distribute vaccine”. Competing poultry health companies have the capacity to supply vaccines that would conform to international and U.S. standards of safety and efficacy.

- The USDA has been attempting to eradicate what is essentially a seasonal and regionally endemic disease since early 2022. The Department now recognizes the futility of eradicating an infection that is introduced and disseminated by millions of migratory birds. The most effective biosecurity is less than absolutely effective given the growing reality that the infection can be transmitted over relatively short distances by the aerogenous route.

During the 2024 IPPE, reports were received on studies conducted by the Agricultural Research Service of the USDA on evaluating alternative vaccines. The presentation by the senior ARS scientist concerned was pitched inappropriately and delivered at a level defying comprehension by members of the United Egg Producers. This commentator, who was also bemused by the rapid series of power points and considerations of complex molecular biology, was reminded of the statement by Albert Einstein “if you can’t explain what you are doing to a ten-year old, maybe you do not know what you are actually doing.”

A recurrence of HPAI that is almost inevitable in the spring of 2024 and probably later in the fall suggest that an 18-month period to “identify a vaccine” is an unconscionable delay and will cost both the USDA (i.e. taxpayers), producers and above all consumers many billions of dollars if flocks are unprotected.

The USDA is “planning to discuss poultry vaccinations with trading partners amid concerns that other countries could restrict imports of vaccinated U.S. poultry”. There has been a groundswell supporting vaccination including endorsement by the World Organization for Animal Health. The World Health Organization is expressing concern over possible emergence of zoonotic avian influenza given the duration of the panornitic and the extension to a wide range of terrestrial and marine mammals.

Clearly the USDA has been negligent in not preemptively pursuing agreements relating to certification of products from vaccinated flocks destined for export as being free of avian influenza at the time of slaughter. PCR is readily available, and it is now possible to differentiate between vaccinated and infected flocks since there is no imperative to rely on serology as in decades past. Unfortunately, administrators are congenitally incapable of adapting policy to new technology or reversing positions in the face of new evidence.

It is questioned who is advising Secretary Vilsack and whether he is obtaining the best possible information based on current scientific and economic realities. It is possible that APHIS administrators are stuck in a 1990’s time warp and are hidebound by precedent and policy that inhibits consideration of practical and realistic alternatives. To their way of thinking, adoption of a limited industry-segment and regional vaccination program would represent a denial of previous decisions encompassed in the ‘whack-a-mole approach to control of HPAI applied during the 2022-2024 epornitic.

|

|

|

|

View More

|

Top

|

|